European Rigidity and American Elasticity: The Key Investors Can No Longer Ignore

Europe's main economic problem is neither inflation, nor debt, nor demographics. It is rigidity. A rigidity that weighs on growth, weakens the economy during crises, and — above all — explains a large part of the persistent underperformance of European assets.

Modern economies move to the rhythm of liquidity and credit cycles. Since the global financial crisis, the ability of a system to inject liquidity quickly and absorb shocks — its financial elasticity — has become a cornerstone of macroeconomic stability. This elasticity largely explains why the world's largest economy has enjoyed almost uninterrupted growth for the past fifteen years.

At first, this elasticity was monetary. Central banks opened the taps through quantitative easing. It later became fiscal. Governments supported growth through debt, which was immediately transformed into liquidity by financial markets.

For investors, the message is straightforward: liquidity is the fuel of markets. It explains the high valuations of U.S. equities, the speed of recoveries, and the economy's ability to absorb shocks.

Growth and Crises: Two Different Worlds

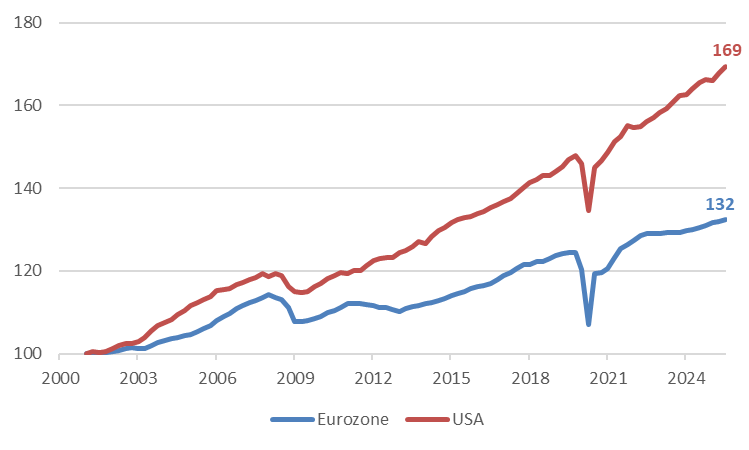

The contrast with Europe is stark. Since the introduction of the euro in 2001, U.S. real GDP has increased by 69%, compared with just 32% in the euro area — twice as much growth over the same period.

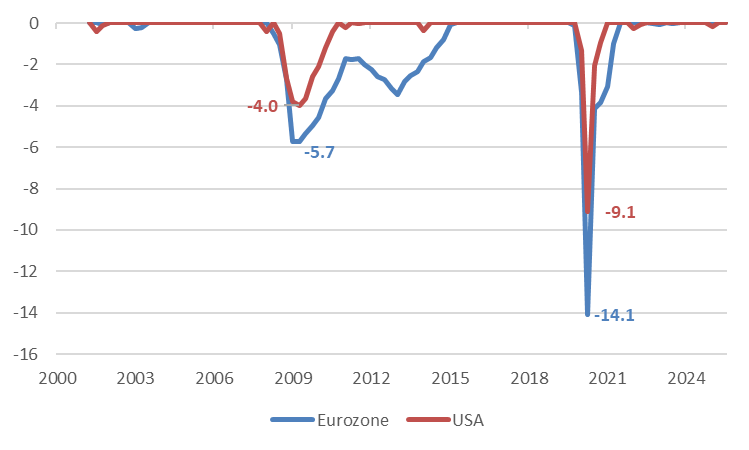

The gap becomes even more striking during crises. In 2008, the U.S. economy contracted by 4%, versus 5.7% in the euro area, before rebounding quickly. Europe, by contrast, became mired in the sovereign debt crisis. The same pattern emerged during COVID: −9.1% in the United States versus −14.1% in the euro area, followed by a much faster recovery across the Atlantic.

This is no coincidence. It reflects radically different financial structures and institutions.

In the United States, companies are largely financed through bond markets. Federal government debt — deep, unified, and highly liquid — forms the backbone of the financial system. Liquidity circulates quickly, everywhere, all the time.

In Europe, financing remains largely bank-based. Capital markets are fragmented and public debt remains national. The result is a system that is less fluid, less reactive, and more vulnerable to shocks — and, for investors, structurally disadvantaged risk assets.

Rigidity or Discipline? Europe's Mistake

The euro area has moved from one crisis to the next. In its quest for credibility, it has too often chosen the strict application of rules, confusing discipline with rigidity. Yet discipline is not the absence of flexibility; it is the ability to adapt rules to achieve a clear objective.

When Mario Draghi delivered his famous "Whatever it takes" speech in 2012, he embodied this intelligent discipline: respecting the framework but using it boldly to protect what mattered most. Fifteen years later, Europe still struggles to turn that moment into a lasting model.

Economically, financially, fiscally, and politically weak, Europe becomes rigid — and therefore fragile. By contrast, American strength allows flexibility: changing rules, bending frameworks, and mobilizing resources rapidly to stabilize the economy.

What Does This Mean for Investors?

European rigidity is not entirely negative. It weighs on equities and real estate, but it supports the currency and bonds, which tend to benefit from strict discipline.

Conversely, U.S. financial elasticity favours equities and real estate, at the cost of massive money creation and a potential long-term weakening of the currency.

Europe is not a failed version of the United States. It is a different financial regime, with distinct strengths, weaknesses, and opportunities.

For investors, the real question is not which side to choose, but which financial regime supports which asset class — and at what stage of the cycle. Because pull an elastic band too far and it snaps. But make the foundation too rigid, and it eventually cracks.

This article is a translation of a column originally published in French on Allnews.ch.

← All publications